Are Index Funds Right for You?

A fundamental decision every stock investor makes is whether to attempt to beat the market or to be content to merely match the market.

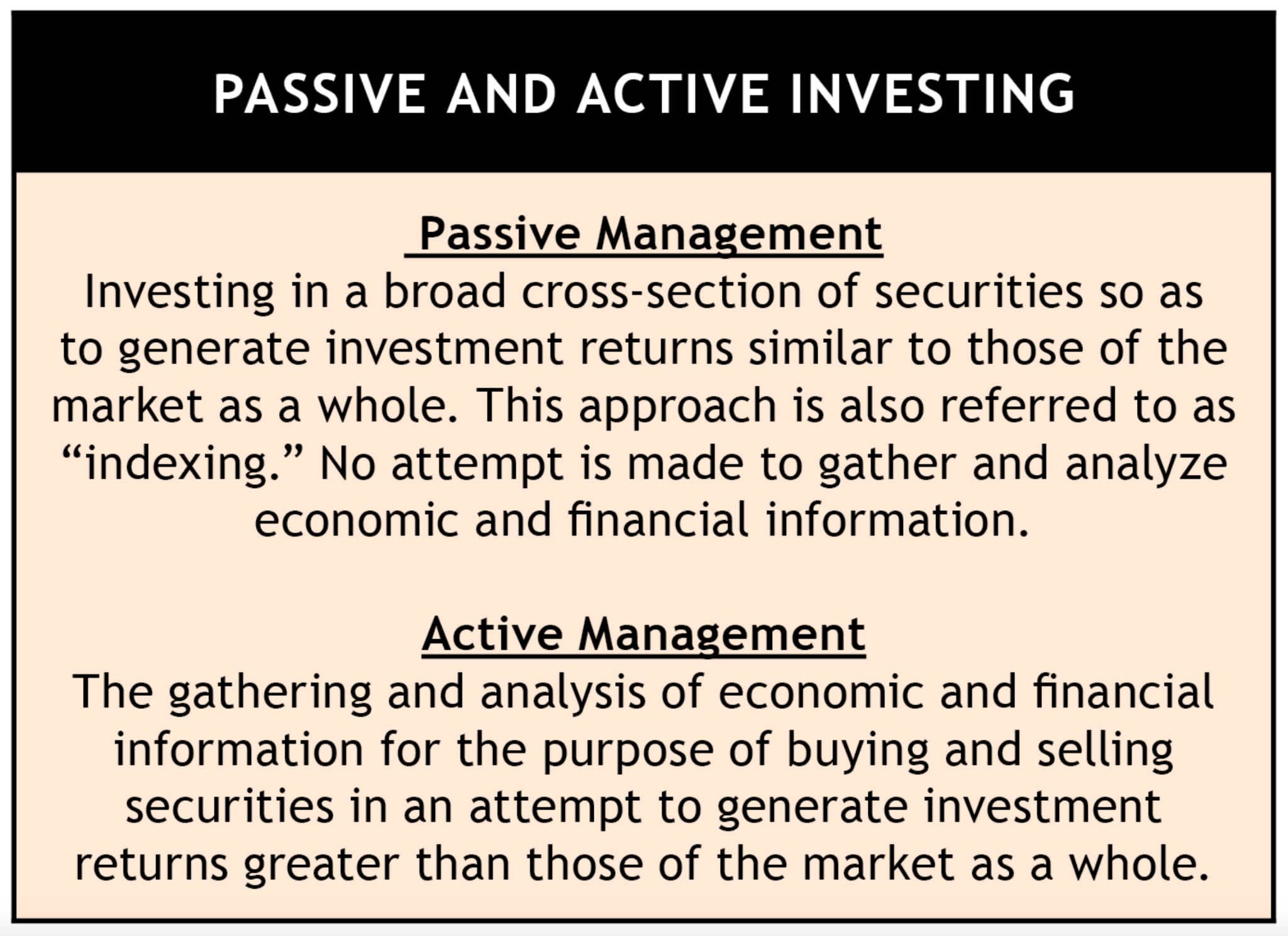

To try to beat the market, you must use actively managed funds — that is, funds that frequently trade stocks in an effort to hold only those that will are performing well.

To merely match the market’s returns, you can use passively managed “index” funds that make no attempt to discern how specific stocks will perform, opting instead to buy the entire group of stocks that make up an index, such as the S&P 500. In doing so, the indexer is willing to accept whatever the market rate of return is (over the long haul, stocks have returned 7%-10% per year).

The Advantages of Index Funds

• Simplicity. Index funds are great for beginners because they’re low maintenance. You don’t have to know anything about picking funds or diversification strategies; just buy a fund like Vanguard’s Total Stock Market fund and — presto! — you own a share in the entire U.S. market. And after you make your investment, there are no monitoring or fine-tuning chores for the next 12 months until it’s time for your annual rebalancing (to make sure the stock/bond mix in your whole portfolio is what you want it to be).

• Predictability. You can buy and hold index funds for years because their performance is predictable — you’ll get what the market gives. While you know you won’t outperform the market, you also know you won’t lag the market either.

• Availability. Index funds are offered as investment options in most employer-sponsored retirement plans, such as 401(k) and 403(b) plans.

Other Considerations

Not all such funds all created equal. When shopping for index funds, it’s crucial that you pay attention to two particulars.

First, find out which index a fund is attempting to replicate. Only a fund that tracks the entire market (such as the Vanguard Total Stock Market Index fund) will give you the “market-matching” returns we’ve been talking about. So if that’s your desire, stick with that fund (or a combination such as an S&P 500 fund and an Extended Market fund that, together, essentially cover the entire market).

In contrast, many index funds track only a certain segment of the market. Their returns will reflect that segment and may be more or less than the overall market.

Secondly, pay attention to fund expenses. The returns from index funds will vary depending on the fees and overhead the fund passes on to shareholders. Even among index funds focused on the same target, there can be significant performance differences due to costs.

The best index funds not only closely track their target index but also keep their costs low. For example, the S&P 500 index fund from industry-leading Vanguard charges just 0.04% per year (that works out to just $4 a year on a $10,000 investment). Higher-cost index funds abound, so don’t assume a particular index fund has low expenses.

Determining if an index fund is a good performer isn’t difficult. Simply compare the posted returns of a particular fund against those of the comparable Vanguard index fund (comparing two S&P 500 funds, for example). If returns are similar over both short and long-term periods, chances the fund you’re considering is a suitable alternative.

The Main Disadvantage of Index Funds

• No protection during periods of market weakness. One of indexing’s greatest strengths during bull markets turns into its biggest weakness during bear markets. Remember, the goal of an index fund is to match the performance of the stock index the fund is tracking.

If the market goes through a steep bear market, index funds typically absorb the full brunt of it. This makes indexing a tougher strategy to stick with emotionally than one might expect. Every time a bear market rolls around and index funds are falling more than other alternatives, the siren song to “abandon ship” will ring loudly in your ears.

So if you’re going to be an indexer, you’ve got to make up your mind to stick with it. If you can do that, you’re likely to get good results over the long term.

*******

Austin Pryor is the founder of Sound Mind Investing, publisher of America's best-selling investment newsletter written from a biblical perspective. He is the author, along with SMI’s Mark Biller, of The Sound Mind Investing Handbook (Moody Publishers), now in its 7th edition.

© Sound Mind Investing